Financial highlights

Revenue

(2024: €1,877m)

Cash generated from operations

(2024: €668m)

EBITDA

(2024: €728m)

Capital expenditure

(2024: €471m)

Net income

(2024: €180m)

Net cash

(2024: €893m)

Met 100% of our customer deliveries.

60% reduction in carbon emissions (scope 1 and 2) from our baseline year of 2019. 5% reduction (scope 3) from our baseline year of 2019.

Enriched enough uranium to generate an estimated 750,000 GWh of electricity from nuclear power, avoiding approximately 380 million tonnes of carbon emissions.

New partnership with the Royal Institution London to further the UK’s scientific education efforts.

Sustainability at Urenco means delivering for a net zero world whilst minimising our own impact on the environment, operating in an open and accountable manner and supporting our local communities. See our near term net zero targets approved by the SBTi.

Belgium

Belgium began the year with six reactors supplying around 55% of the nation’s electricity. In 2025, several units were permanently shut down: Doel-1, Tihange-1, and Doel-2. While Belgium had originally planned to close all reactors by the end of 2025, legislative changes allowed for the continued operation of Doel-4 and Tihange-3. In September, reports indicated that Engie was willing to consider extending the operation of the Doel-4 and Tihange-3 nuclear reactors by 20 years, up from the previously agreed 10-year extension which had been finalised in March.

France

In July, EDF announced that it would provide details of a plan for eight new reactors by the end of 2026, following a final investment decision on six reactors already in the planning stage. However, highlighting the ongoing challenges of constructing new nuclear facilities, the Government reported in March that the first commissioning of one of those six EPR2 reactors is now scheduled for 2038, delayed from the previously planned 2035.

Italy

In October, Italy’s Council of Ministers approved a bill delegating authority for the reintroduction of nuclear energy, as the Government seeks to lift the ban on reactors. The bill, which still requires parliamentary approval, would empower the Government to regulate the development of nuclear power within the framework of European decarbonisation and energy security policies. Earlier in the year, Edison, the Italian arm of EDF, announced plans to build two advanced reactors by 2040, with the first unit targeted for completion in 2035 and the second in 2040.

Netherlands

In October 2025, the Dutch Government formally submitted an amendment to the Nuclear Energy Act to Parliament that would allow the Borssele nuclear power plant to operate well beyond its current planned closure in 2033 – potentially until 2054 if safety conditions are met.

Meanwhile, Dutch authorities have also expanded potential sites for two nuclear reactors and potentially two additional reactors. These include locations such as Tweede Maasvlakte (Rotterdam) and Terneuzen. However, because of this additional required work, the Government acknowledged that the earlier 2035 target for bringing the first new large reactor into operation will be difficult to meet. The new Dutch government took office on February 23 and will continue the nuclear programme.

Poland

In December, the European Commission concluded that Poland’s planned public support for its first largescale nuclear power plant complies with EU state aid rules, paving the way for the Government to sign a construction contract with a consortium of American companies led by Westinghouse. Poland aims to begin construction of the first unit of the plant in 2028 and complete it in 2036.

Complementing this flagship project, Poland is also moving into SMRs. In August, it selected Włocławek as the site for its first SMR installation, where it plans to deploy two 300MW GE Hitachi BWRX-300 units by 2035, underscoring the country’s dual strategy of combining traditional nuclear capacity with emerging modular technologies.

Slovak Republic

Slovakia has approved an agreement with the United States to build an additional nuclear reactor at the existing site in Jaslovské Bohunice. The planned reactor will have an output of over 1GW and be fully owned by the state.

Hungary

Hungary plans to begin construction of the Paks II nuclear plant in February 2026, with the first of two Russianbuilt reactors expected online in the early 2030s. At the same time, life extension work on the existing Paks plant, comprising four units, is proceeding.

Spain

In what could be seen as a positive sign for the future of nuclear power in Spain, the owners of the Almaraz nuclear power plant have requested an extension of operations until 2030. Notably, they have withdrawn their request for a nuclear-energy tax break, a key point of contention with the Government in their bid to extend the life of the two units. Almaraz-1 and -2 are currently scheduled to shut down in November 2027 and October 2028, respectively, marking the beginning of Spain’s planned phase-out of nuclear power by 2035.

By dropping their requests for tax relief and making an unconditional offer to continue operating, the owners have effectively met the Government’s first ‘red line’. Attention will now shift to the second red line, ensuring plant safety, which is reportedly under review. The third concerns maintaining security of electricity supply, an issue that will come into sharper focus if the extension moves forward.

Sweden

In May, Sweden's parliament passed legislation to finance a new generation of nuclear reactors that the Government views as essential for energy security and achieving net zero emissions by 2045. The plan envisions four large scale reactors - totalling around 5GW of capacity - or an equivalent amount delivered through SMRs, with half of the new capacity targeted to be online by 2035.

Complementing the Government’s wider push for new nuclear capacity, Vattenfall reported in August that it had decided to pursue SMRs for its next phase of development. The company aims to deploy new capacity on the Värö Peninsula, home to the Ringhals nuclear power plant, in the early 2030s. The project is planned for 1.5GW of capacity.

Later in the year, Sweden reinforced this broader nuclear strategy by addressing fuel-supply constraints. In November, parliament lifted the country’s long standing ban on uranium mining as part of its effort to support new reactor construction.

UK

In February, the UK Government announced plans to expand nuclear power, pledging to open additional sites nationwide for new power stations. This builds on the Government’s push for technology companies to collaborate on developing SMRs capable of powering energy-intensive AI datacentres across Britain. As part of this wider expansion plan, the Government will, for the first time, allow nuclear projects to be developed outside the eight previously designated sites. Complementing this shift, forthcoming planning reforms are intended to speed up the rollout of SMRs.

In June, Great British Energy-Nuclear, the public-sector body responsible for supporting new nuclear projects under the UK’s clean energy plans, selected Rolls- Royce SMR as the preferred bidder to build the UK’s first SMR. The programme aims to reach a final investment decision in 2029, with initial units expected online in the mid- 2030s. The Government confirmed Wylfa in North Wales as the chosen site, where three Rolls-Royce SMR units are planned. Early works are expected to begin around 2026.

In July, the UK signed the final investment decision for the Sizewell C nuclear power plant and became the largest shareholder in the £38 billion project alongside EDF, Centrica, La Caisse and Amber Infrastructure.

In September, X-Energy and Centrica announced plans to build up to 12 advanced modular reactors in Hartlepool, with a follow-on UK wide programme targeting a fleet of 6GW of nuclear power. According to the companies, the Hartlepool project would generate enough power for up to 1.5 million homes and create up to 2,500 jobs.

However, a government review published in November highlighted significant challenges for nuclear new build in the UK . The Prime Minister has accepted the principle of the report’s recommendations , including a new Commission for Nuclear Regulation.

Canada

The Province of Ontario has given Ontario Power Generation (OPG) the approval to start construction of the first of four GE Hitachi BWRX-300 SMRs planned at the Darlington New Nuclear Project site. Expected to come online in 2030, it will be the first new nuclear build in Ontario in more than three decades and the first commercial grid-scale SMR in North America.

USA

Strong bipartisan support sustained the USA’s rapid nuclear momentum in 2025, spanning fleet extensions, restarts of shuttered units, and announcements of new projects, including both large reactors and advanced designs.

In May, President Trump signed four executive orders aimed at quadrupling US nuclear capacity by 2050, accelerating reactor approvals, strengthening domestic uranium production and enrichment, and boosting deployment of advanced nuclear technologies. The orders direct the DOE to support the start of construction on ten large reactors by 2030, finance power uprates across the existing fleet, and implement a “wholesale revision” of NRC rules and guidelines.

Following the executive orders, Westinghouse announced plans to build ten large reactors in the US, targeting construction by 2030. Later in the year, Westinghouse’s owners, Cameco and Brookfield Asset Management, announced a strategic partnership with the federal Government, aligned with the executive orders, targeting at least $80 billion of new reactors.

NextEra Energy plans to restart the Duane Arnold Energy Centre in Iowa, with full operation targeted by Q1 2029, supported by a Google power purchase agreement to supply cloud and AI operations. The plant originally shut down in 2020 after it was deemed no longer economically viable under market conditions at the time.

Constellation reports that its project to restart Three Mile Island-1 in Pennsylvania, renamed the Crane Clean Energy Center (CCEC), remains ahead of schedule, with the unit expected back online in 2027. The plant was approved for restart in 2024 and is underpinned by a 20-year agreement with Microsoft to power its data centres.

Technology companies continue to drive strong demand for nuclear energy. In June, Meta signed a 20-year contract to purchase output from Constellation’s Clinton nuclear plant starting mid-2027, securing the plant’s long-term future. In the same month, Talen Energy entered a power purchase agreement through 2042 for 1.92GW of carbon-free electricity to support Amazon’s AI and cloud operations, while exploring SMR options.

New build and expansion projects elsewhere are also progressing. In October, Brookfield signed a letter of intent with Santee Cooper to explore purchasing and completing the two unfinished AP1000 reactors at V.C. Summer which advanced to a formal MOU for a feasibility study with a target final investment decision by June 2026. If completed, the units could generate more than 2GW of carbon-free power.

Meanwhile, the New York Power Authority issued its first call for proposals to develop advanced nuclear reactors in upstate communities, aiming to add at least 1GW of capacity by 2040. In November, Constellation proposed a range of measures for the Calvert Cliffs Clean Energy Center, including 20 year life extensions for its two existing units.

The US Government itself moved quickly in 2025 to accelerate the development of advanced reactors. In May, Kairos Power completed the first installation of nuclear safety-related concrete for the Hermes Low-Power Demonstration Reactor in Oak Ridge, Tennessee, the first advanced reactor to receive an NRC construction permit, marking the start of “nuclear construction”. In July, the DOE was mandated to authorise and develop three pilot SMRs to meet surging AI demand, aiming for “criticality” by July 2026, while the Department of Defense was directed to commission its own pilot reactor within three years. At the same time, the NRC completed its environmental review and safety evaluation of TerraPower’s Natrium reactor outside Kemmerer. The plant is still projected to come online around 2030.

In November, Valar Atomics achieved criticality, becoming the first nuclear startup to create a critical fission reaction under the DOE pilot program established following the May executive orders.

China

In April, the Chinese Government approved another ten nuclear reactors across five sites – this takes total approvals to 41 units in the last four years. Meanwhile, Zhangzhou-1, the first unit at Zhangzhou Nuclear Power Plant began commercial operation in January 2025. Zhangzhou-2 is expected to enter commercial operation soon.

Taiwan

In May, Taiwan shut down its last operational nuclear reactor, Maanshan-2, after its operating licence expired. The closure fulfilled the long-standing “nuclear-free homeland” policy, first outlined in 2016 and codified in law as a complete phase-out of nuclear power by 2025.

However, shortly before the shutdown, the legislature amended the Nuclear Reactor Facilities Regulation Act to allow decommissioned plants to apply for licence extensions or reoperation under updated safety and review procedures. In November, the Ministry of Economic Affairs (MOEA) assessed the decommissioned facilities and concluded that at least some, including Maanshan, remain “feasible for reoperation”. The MOEA has indicated that reactors could potentially restart as early as 2028, pending safety reviews, effectively opening the door to reversing the phaseout policy.

Japan

In July, nuclear operator Kansai Electric Power Company announced it will begin surveys for a new reactor at its Mihama power station in Fukui prefecture, Western Japan, intended to replace the existing facility. This marks Japan’s first concrete step toward building a new nuclear reactor since 2011. Kansai Electric had been studying a successor to the Mihama-1 reactor since November 2010 but suspended the project after 2011.

This announcement follows the Government’s February revision of its Basic Energy Plan, which now allows electric power companies that have decommissioned nuclear plants to construct new reactors on the sites of other existing nuclear facilities under a “reconstruction” framework.

Meanwhile, restarts of Japan’s existing fleet are progressing steadily. Shimane-2 returned to commercial operation in January, while Kashiwazaki Kariwa-6 and Tomari-3 have received restart approvals and are targeting returns to service in 2026 and 2027, respectively.

South Korea

In February, South Korea cancelled one of three planned large reactors following the impeachment of pro-nuclear former president Yoon Suk Yeol. His removal shifted political influence toward the renewables-oriented opposition, prompting a reduction in the country’s nuclear expansion plans: the target for new nuclear capacity by 2038 was cut from 4.9 GW to 3.5 GW. Even so, the Government continues to pursue new technologies, including SMR projects with total capacity of around 700 MW, aiming for completion by 2036.

Progress on existing projects has continued as well. In May, KHNP announced the pouring of first concrete for Shin Hanul-3, with completion expected in 2032. Another significant development came in November, when the Nuclear Safety and Security Commission approved a 10-year life extension for Kori-2, the country’s oldest operating reactor. Kori-2 had been shut down in April 2023 after reaching the end of its original 40-year design life, and the extension will allow it to operate until April 2033. This marks a major policy shift, potentially opening the door to similar extensions for up to nine other ageing reactors as concerns grow about future power supply shortages amid rising electricity demand.

-

Belgium

Belgium

Belgium began the year with six reactors supplying around 55% of the nation’s electricity. In 2025, several units were permanently shut down: Doel-1, Tihange-1, and Doel-2. While Belgium had originally planned to close all reactors by the end of 2025, legislative changes allowed for the continued operation of Doel-4 and Tihange-3. In September, reports indicated that Engie was willing to consider extending the operation of the Doel-4 and Tihange-3 nuclear reactors by 20 years, up from the previously agreed 10-year extension which had been finalised in March.

-

France

France

In July, EDF announced that it would provide details of a plan for eight new reactors by the end of 2026, following a final investment decision on six reactors already in the planning stage. However, highlighting the ongoing challenges of constructing new nuclear facilities, the Government reported in March that the first commissioning of one of those six EPR2 reactors is now scheduled for 2038, delayed from the previously planned 2035.

-

Italy

In October, Italy’s Council of Ministers approved a bill delegating authority for the reintroduction of nuclear energy, as the Government seeks to lift the ban on reactors. The bill, which still requires parliamentary approval, would empower the Government to regulate the development of nuclear power within the framework of European decarbonisation and energy security policies. Earlier in the year, Edison, the Italian arm of EDF, announced plans to build two advanced reactors by 2040, with the first unit targeted for completion in 2035 and the second in 2040.

-

Netherlands

In October 2025, the Dutch Government formally submitted an amendment to the Nuclear Energy Act to Parliament that would allow the Borssele nuclear power plant to operate well beyond its current planned closure in 2033 – potentially until 2054 if safety conditions are met.

Meanwhile, Dutch authorities have also expanded potential sites for two nuclear reactors and potentially two additional reactors. These include locations such as Tweede Maasvlakte (Rotterdam) and Terneuzen. However, because of this additional required work, the Government acknowledged that the earlier 2035 target for bringing the first new large reactor into operation will be difficult to meet. The new Dutch government took office on February 23 and will continue the nuclear programme. -

Poland

Poland

In December, the European Commission concluded that Poland’s planned public support for its first largescale nuclear power plant complies with EU state aid rules, paving the way for the Government to sign a construction contract with a consortium of American companies led by Westinghouse. Poland aims to begin construction of the first unit of the plant in 2028 and complete it in 2036.

Complementing this flagship project, Poland is also moving into SMRs. In August, it selected Włocławek as the site for its first SMR installation, where it plans to deploy two 300MW GE Hitachi BWRX-300 units by 2035, underscoring the country’s dual strategy of combining traditional nuclear capacity with emerging modular technologies.

-

Slovak Republic

Slovakia has approved an agreement with the United States to build an additional nuclear reactor at the existing site in Jaslovské Bohunice. The planned reactor will have an output of over 1GW and be fully owned by the state.

-

Hungary

Hungary plans to begin construction of the Paks II nuclear plant in February 2026, with the first of two Russianbuilt reactors expected online in the early 2030s. At the same time, life extension work on the existing Paks plant, comprising four units, is proceeding.

-

Spain

In what could be seen as a positive sign for the future of nuclear power in Spain, the owners of the Almaraz nuclear power plant have requested an extension of operations until 2030. Notably, they have withdrawn their request for a nuclear-energy tax break, a key point of contention with the Government in their bid to extend the life of the two units. Almaraz-1 and -2 are currently scheduled to shut down in November 2027 and October 2028, respectively, marking the beginning of Spain’s planned phase-out of nuclear power by 2035.

By dropping their requests for tax relief and making an unconditional offer to continue operating, the owners have effectively met the Government’s first ‘red line’. Attention will now shift to the second red line, ensuring plant safety, which is reportedly under review. The third concerns maintaining security of electricity supply, an issue that will come into sharper focus if the extension moves forward.

-

Sweden

Sweden

In May, Sweden's parliament passed legislation to finance a new generation of nuclear reactors that the Government views as essential for energy security and achieving net zero emissions by 2045. The plan envisions four large scale reactors - totalling around 5GW of capacity - or an equivalent amount delivered through SMRs, with half of the new capacity targeted to be online by 2035.

Complementing the Government’s wider push for new nuclear capacity, Vattenfall reported in August that it had decided to pursue SMRs for its next phase of development. The company aims to deploy new capacity on the Värö Peninsula, home to the Ringhals nuclear power plant, in the early 2030s. The project is planned for 1.5GW of capacity.

Later in the year, Sweden reinforced this broader nuclear strategy by addressing fuel-supply constraints. In November, parliament lifted the country’s long standing ban on uranium mining as part of its effort to support new reactor construction.

-

UK

In February, the UK Government announced plans to expand nuclear power, pledging to open additional sites nationwide for new power stations. This builds on the Government’s push for technology companies to collaborate on developing SMRs capable of powering energy-intensive AI datacentres across Britain. As part of this wider expansion plan, the Government will, for the first time, allow nuclear projects to be developed outside the eight previously designated sites. Complementing this shift, forthcoming planning reforms are intended to speed up the rollout of SMRs.

In June, Great British Energy-Nuclear, the public-sector body responsible for supporting new nuclear projects under the UK’s clean energy plans, selected Rolls- Royce SMR as the preferred bidder to build the UK’s first SMR. The programme aims to reach a final investment decision in 2029, with initial units expected online in the mid- 2030s. The Government confirmed Wylfa in North Wales as the chosen site, where three Rolls-Royce SMR units are planned. Early works are expected to begin around 2026.

In July, the UK signed the final investment decision for the Sizewell C nuclear power plant and became the largest shareholder in the £38 billion project alongside EDF, Centrica, La Caisse and Amber Infrastructure.

In September, X-Energy and Centrica announced plans to build up to 12 advanced modular reactors in Hartlepool, with a follow-on UK wide programme targeting a fleet of 6GW of nuclear power. According to the companies, the Hartlepool project would generate enough power for up to 1.5 million homes and create up to 2,500 jobs.

However, a government review published in November highlighted significant challenges for nuclear new build in the UK . The Prime Minister has accepted the principle of the report’s recommendations , including a new Commission for Nuclear Regulation.

-

Canada

Canada

The Province of Ontario has given Ontario Power Generation (OPG) the approval to start construction of the first of four GE Hitachi BWRX-300 SMRs planned at the Darlington New Nuclear Project site. Expected to come online in 2030, it will be the first new nuclear build in Ontario in more than three decades and the first commercial grid-scale SMR in North America.

-

USA

USA

Strong bipartisan support sustained the USA’s rapid nuclear momentum in 2025, spanning fleet extensions, restarts of shuttered units, and announcements of new projects, including both large reactors and advanced designs.

In May, President Trump signed four executive orders aimed at quadrupling US nuclear capacity by 2050, accelerating reactor approvals, strengthening domestic uranium production and enrichment, and boosting deployment of advanced nuclear technologies. The orders direct the DOE to support the start of construction on ten large reactors by 2030, finance power uprates across the existing fleet, and implement a “wholesale revision” of NRC rules and guidelines.

Following the executive orders, Westinghouse announced plans to build ten large reactors in the US, targeting construction by 2030. Later in the year, Westinghouse’s owners, Cameco and Brookfield Asset Management, announced a strategic partnership with the federal Government, aligned with the executive orders, targeting at least $80 billion of new reactors.

NextEra Energy plans to restart the Duane Arnold Energy Centre in Iowa, with full operation targeted by Q1 2029, supported by a Google power purchase agreement to supply cloud and AI operations. The plant originally shut down in 2020 after it was deemed no longer economically viable under market conditions at the time.

Constellation reports that its project to restart Three Mile Island-1 in Pennsylvania, renamed the Crane Clean Energy Center (CCEC), remains ahead of schedule, with the unit expected back online in 2027. The plant was approved for restart in 2024 and is underpinned by a 20-year agreement with Microsoft to power its data centres.

Technology companies continue to drive strong demand for nuclear energy. In June, Meta signed a 20-year contract to purchase output from Constellation’s Clinton nuclear plant starting mid-2027, securing the plant’s long-term future. In the same month, Talen Energy entered a power purchase agreement through 2042 for 1.92GW of carbon-free electricity to support Amazon’s AI and cloud operations, while exploring SMR options.

New build and expansion projects elsewhere are also progressing. In October, Brookfield signed a letter of intent with Santee Cooper to explore purchasing and completing the two unfinished AP1000 reactors at V.C. Summer which advanced to a formal MOU for a feasibility study with a target final investment decision by June 2026. If completed, the units could generate more than 2GW of carbon-free power.

Meanwhile, the New York Power Authority issued its first call for proposals to develop advanced nuclear reactors in upstate communities, aiming to add at least 1GW of capacity by 2040. In November, Constellation proposed a range of measures for the Calvert Cliffs Clean Energy Center, including 20 year life extensions for its two existing units.

The US Government itself moved quickly in 2025 to accelerate the development of advanced reactors. In May, Kairos Power completed the first installation of nuclear safety-related concrete for the Hermes Low-Power Demonstration Reactor in Oak Ridge, Tennessee, the first advanced reactor to receive an NRC construction permit, marking the start of “nuclear construction”. In July, the DOE was mandated to authorise and develop three pilot SMRs to meet surging AI demand, aiming for “criticality” by July 2026, while the Department of Defense was directed to commission its own pilot reactor within three years. At the same time, the NRC completed its environmental review and safety evaluation of TerraPower’s Natrium reactor outside Kemmerer. The plant is still projected to come online around 2030.

In November, Valar Atomics achieved criticality, becoming the first nuclear startup to create a critical fission reaction under the DOE pilot program established following the May executive orders.

-

China

China

In April, the Chinese Government approved another ten nuclear reactors across five sites – this takes total approvals to 41 units in the last four years. Meanwhile, Zhangzhou-1, the first unit at Zhangzhou Nuclear Power Plant began commercial operation in January 2025. Zhangzhou-2 is expected to enter commercial operation soon.

-

Taiwan

In May, Taiwan shut down its last operational nuclear reactor, Maanshan-2, after its operating licence expired. The closure fulfilled the long-standing “nuclear-free homeland” policy, first outlined in 2016 and codified in law as a complete phase-out of nuclear power by 2025.

However, shortly before the shutdown, the legislature amended the Nuclear Reactor Facilities Regulation Act to allow decommissioned plants to apply for licence extensions or reoperation under updated safety and review procedures. In November, the Ministry of Economic Affairs (MOEA) assessed the decommissioned facilities and concluded that at least some, including Maanshan, remain “feasible for reoperation”. The MOEA has indicated that reactors could potentially restart as early as 2028, pending safety reviews, effectively opening the door to reversing the phaseout policy.

-

Japan

Japan

In July, nuclear operator Kansai Electric Power Company announced it will begin surveys for a new reactor at its Mihama power station in Fukui prefecture, Western Japan, intended to replace the existing facility. This marks Japan’s first concrete step toward building a new nuclear reactor since 2011. Kansai Electric had been studying a successor to the Mihama-1 reactor since November 2010 but suspended the project after 2011.

This announcement follows the Government’s February revision of its Basic Energy Plan, which now allows electric power companies that have decommissioned nuclear plants to construct new reactors on the sites of other existing nuclear facilities under a “reconstruction” framework.

Meanwhile, restarts of Japan’s existing fleet are progressing steadily. Shimane-2 returned to commercial operation in January, while Kashiwazaki Kariwa-6 and Tomari-3 have received restart approvals and are targeting returns to service in 2026 and 2027, respectively.

-

South Korea

South Korea

In February, South Korea cancelled one of three planned large reactors following the impeachment of pro-nuclear former president Yoon Suk Yeol. His removal shifted political influence toward the renewables-oriented opposition, prompting a reduction in the country’s nuclear expansion plans: the target for new nuclear capacity by 2038 was cut from 4.9 GW to 3.5 GW. Even so, the Government continues to pursue new technologies, including SMR projects with total capacity of around 700 MW, aiming for completion by 2036.

Progress on existing projects has continued as well. In May, KHNP announced the pouring of first concrete for Shin Hanul-3, with completion expected in 2032. Another significant development came in November, when the Nuclear Safety and Security Commission approved a 10-year life extension for Kori-2, the country’s oldest operating reactor. Kori-2 had been shut down in April 2023 after reaching the end of its original 40-year design life, and the extension will allow it to operate until April 2033. This marks a major policy shift, potentially opening the door to similar extensions for up to nine other ageing reactors as concerns grow about future power supply shortages amid rising electricity demand.

- Over 2,700 highly skilled and well-trained employees

- Leading centrifuge technology

- Excellence in safety and maintenance

- Innovation and R&D

- Strong customer service

- Rigorous supplier and compliance audits

- Detailed market intelligence

- Robust commitment to nuclear safeguards and non-proliferation through the Treaties of Almelo, Washington and Cardiff, and government oversight

- Integrated and diverse nuclear fuel supplier helping to deliver energy security and independence

- Capacity programme to meet increased demand from our customers

- Evolution of the nuclear fuel cycle through the development of advanced fuels’ services and products, including low-enriched uranium plus (LEU+ – uranium enriched up to 10%) and high-assay, low-enriched uranium (HALEU – uranium enriched up to 20%)

- Commitment to meet net zero emissions by 2040, with a near-term target of a 90% reduction in emissions from our operations (scope 1 and 2) and a 30% reduction in our scope 3 (supply chain) emissions in absolute terms by 2030

- Reliable transatlantic transportation services

- Enhanced and innovative isotopes offering for non-energy purposes, including medical, industrial and research applications

- Responsible nuclear stewardship, including materials management and decommissioning

- Revenue: €2,096 million (2024: €1,877 million)

- EBITDA: €804 million (2024: €728 million)

- Net income: €249 million (2024: €180 million)

- Cash generated from operations: €1,047.4 million (2024: €668 million)

- Capital expenditure: €615.8 million (2024: €471 million)

- Net cash was €845 million (2024: €893 million)

- Contract order book extending into the 2040s, with increased value as of 31 December 2025 of €21.3 billion (€18.7 billion 2024)

- Global enrichment capacity of 17.2 million SWU/year (2024: 17.3 million SWU/year)

- Capacity generates an estimated 750,000GWh of electricity from nuclear power, sufficient for more than 95% of all the households in the EU and UK for one year, or more than 50% of all households in the US for one year

- Capacity avoids approximately 380 million tonnes of carbon emissions

- Serving more than 50 customers in over 20 countries

- 100% of customer deliveries met

- Total Recordable Injury Rate (TRIR) slightly higher at 0.400 (2024: 0.291); resulting in 15 total recordable injuries, all non-nuclear related, although safety performance remains strong compared to external peers.

- Carbon emissions decreased by 15% (scopes 1 and 2 combined – direct and indirect emissions) from 2024, and fell by 60% from 2019 baseline year

- Water withdrawal increased compared to 2024 and against the baseline year of 2020

- Total energy use increased slightly by 0.26% compared to 2024

- New social impact partnership established, further supporting educational goals

Our business strategy

Our strategic ambitions are:

Trusted global partner

Reliable strategic partner to customers, governments and society

Safe, reliable and

efficient operator

A dynamic, learning and responsible nuclear organisation with world class safety, reliability, productivity and efficiency

Engaged and

accountable teams

Inclusive and inspiring place to work, with engaged, accountable, and empowered teams

Expanded and

sustainable assets

Delivering sustainable, net zero assets to meet growing and changing nuclear fuel demand

Industry leading

innovation

Innovating and developing focused opportunities that strengthen and expand our business

-

January 2025 - Urenco extended a social impact partnership with a UK education charity which will result in more STEM teachers being trained." uk-cover>

January 2025 - Urenco extended a social impact partnership with a UK education charity which will result in more STEM teachers being trained." uk-cover>

January 2025 - Urenco extended a social impact partnership with a UK education charity which will result in more STEM teachers being trained." uk-cover>

January 2025 - Urenco extended a social impact partnership with a UK education charity which will result in more STEM teachers being trained." uk-cover>

-

February 2025 - Nuclear Week in Parliament sees MPs and Peers gather to discuss nuclear energy with industry." uk-cover>

February 2025 - Nuclear Week in Parliament sees MPs and Peers gather to discuss nuclear energy with industry." uk-cover>

February 2025 - Nuclear Week in Parliament sees MPs and Peers gather to discuss nuclear energy with industry." uk-cover>

February 2025 - Nuclear Week in Parliament sees MPs and Peers gather to discuss nuclear energy with industry." uk-cover>

-

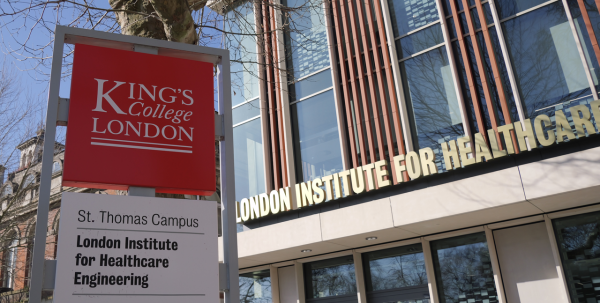

April 2025 - Urenco Isotopes celebrated successful research and development partnership with King’s College London." uk-cover>

April 2025 - Urenco Isotopes celebrated successful research and development partnership with King’s College London." uk-cover>

April 2025 - Urenco Isotopes celebrated successful research and development partnership with King’s College London." uk-cover>

April 2025 - Urenco Isotopes celebrated successful research and development partnership with King’s College London." uk-cover>

-

June 2025 - Members of Urenco’s Young Persons Network (YPN) participated in the European Nuclear Young Generation Forum (ENYGF) in Zagreb. " uk-cover>

June 2025 - Members of Urenco’s Young Persons Network (YPN) participated in the European Nuclear Young Generation Forum (ENYGF) in Zagreb. " uk-cover>

June 2025 - Members of Urenco’s Young Persons Network (YPN) participated in the European Nuclear Young Generation Forum (ENYGF) in Zagreb. " uk-cover>

June 2025 - Members of Urenco’s Young Persons Network (YPN) participated in the European Nuclear Young Generation Forum (ENYGF) in Zagreb. " uk-cover>

-

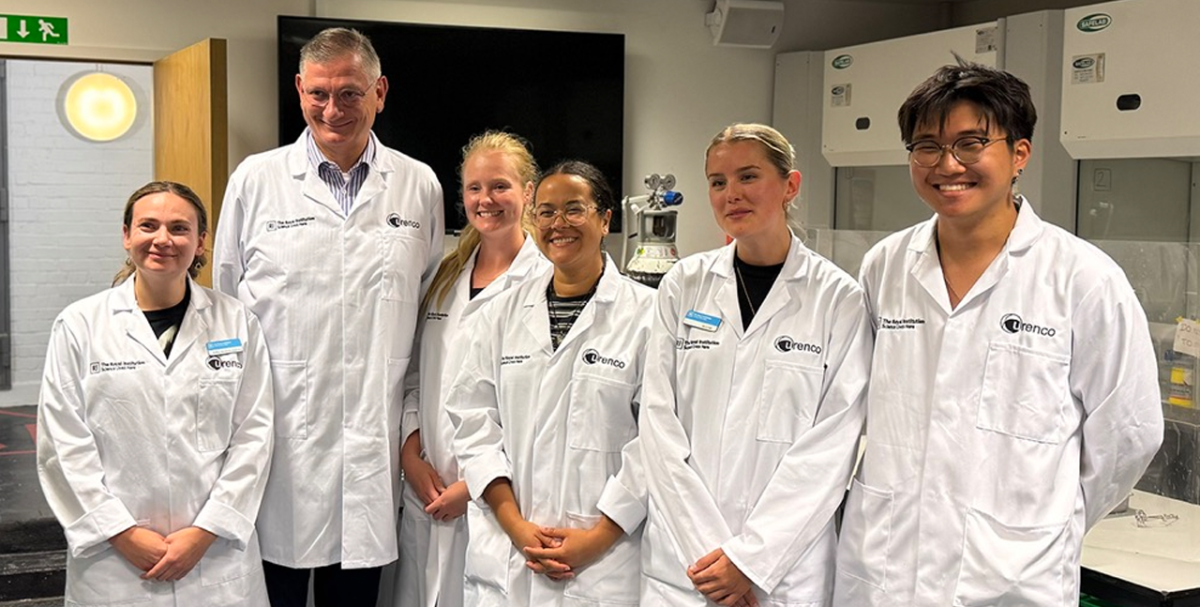

July 2025 - Urenco teamed up with the Royal Institution (Ri) to support its interactive laboratory for young people." uk-cover>

July 2025 - Urenco teamed up with the Royal Institution (Ri) to support its interactive laboratory for young people." uk-cover>

July 2025 - Urenco teamed up with the Royal Institution (Ri) to support its interactive laboratory for young people." uk-cover>

July 2025 - Urenco teamed up with the Royal Institution (Ri) to support its interactive laboratory for young people." uk-cover>

-

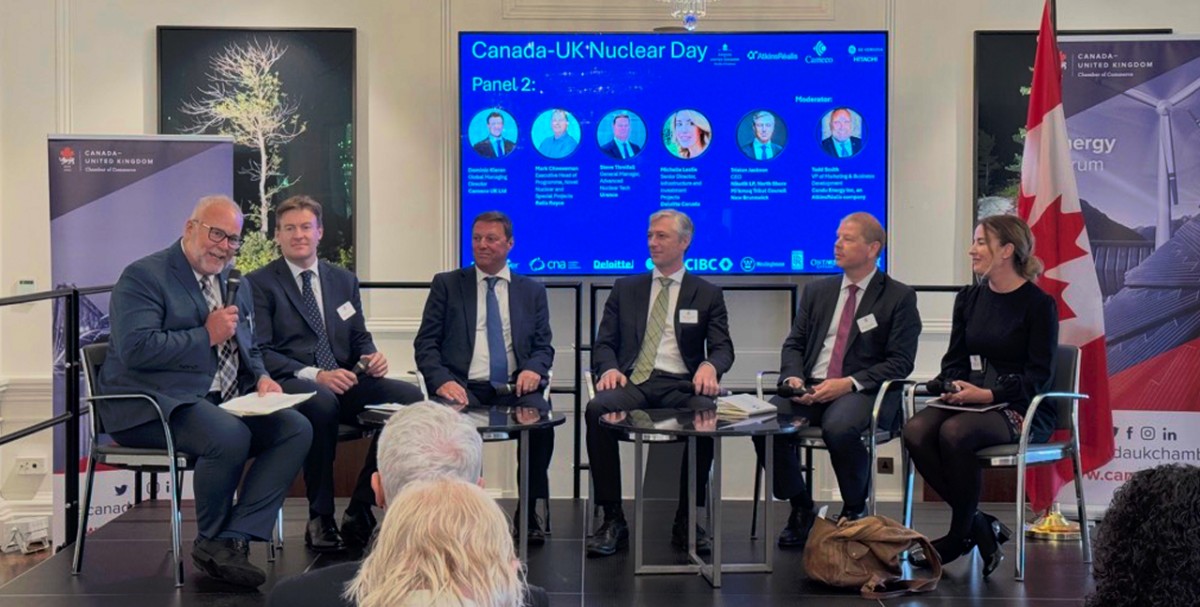

September 2025 - Urenco hosted a nuclear delegation from Canada and took part in a panel at a government-supported event." uk-cover>

September 2025 - Urenco hosted a nuclear delegation from Canada and took part in a panel at a government-supported event." uk-cover>

September 2025 - Urenco hosted a nuclear delegation from Canada and took part in a panel at a government-supported event." uk-cover>

September 2025 - Urenco hosted a nuclear delegation from Canada and took part in a panel at a government-supported event." uk-cover>

-

October 2025 - Further capacity expansion at Urenco’s site in Almelo, the Netherlands." uk-cover>

October 2025 - Further capacity expansion at Urenco’s site in Almelo, the Netherlands." uk-cover>

October 2025 - Further capacity expansion at Urenco’s site in Almelo, the Netherlands." uk-cover>

October 2025 - Further capacity expansion at Urenco’s site in Almelo, the Netherlands." uk-cover>

-

November 2025 - Urenco signed an agreement with EDF to supply uranium enrichment services for nuclear power stations across France and the UK." uk-cover>

November 2025 - Urenco signed an agreement with EDF to supply uranium enrichment services for nuclear power stations across France and the UK." uk-cover>

November 2025 - Urenco signed an agreement with EDF to supply uranium enrichment services for nuclear power stations across France and the UK." uk-cover>

November 2025 - Urenco signed an agreement with EDF to supply uranium enrichment services for nuclear power stations across France and the UK." uk-cover>

-

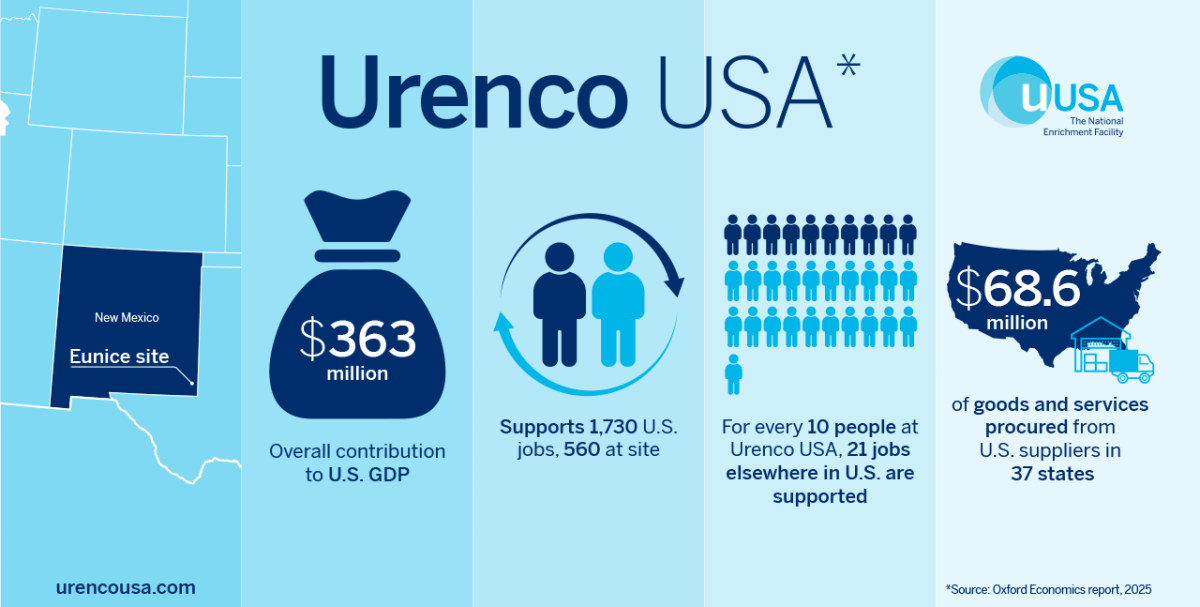

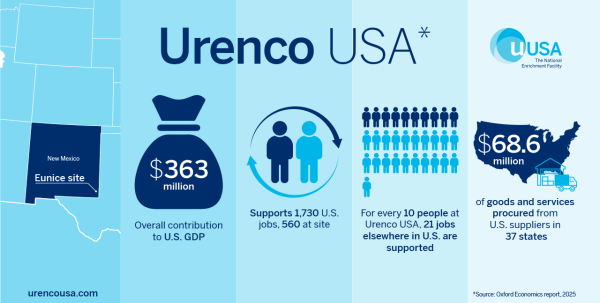

December 2025 - Urenco USA provides significant socioeconomic benefits at the local, regional and national level." uk-cover>

December 2025 - Urenco USA provides significant socioeconomic benefits at the local, regional and national level." uk-cover>

December 2025 - Urenco USA provides significant socioeconomic benefits at the local, regional and national level." uk-cover>

December 2025 - Urenco USA provides significant socioeconomic benefits at the local, regional and national level." uk-cover>